For the first innings of the AI Infrastructure trade, it was simple enough just to know the basics. Large Language Models run on GPUs, buy Nvidia. AI compute will lift optics out of the telecom doghouse and cause significant growth for interconnects, buy the optical interconnect names. Every iota of AI compute demand in the agentic era must inevitably flow through the memory OEMs, buy Micron and SK Hynix.

It seemed a lot more difficult than that at the time, but it was pretty much that simple. The reasons for that were twofold. First, not everyone bought into the massive growth in data centers that would be required for AI to proliferate and actualize. Second, between the post-COVID supply chain glut and numerous other headwinds to semiconductor and adjacent names, valuations remained quite forgiving in all but the most obvious first-order beneficiaries.

That’s begun to change, and with it, outperforming in the AI infrastructure complex requires in-depth understanding beyond just identifying current bottlenecks. Understanding the roadmap for the future requires a bit more technical competence, which is why in January 2026 we began our Semis Memo series – guided by our semis analysts Zephyr and Jukan.

While the landscape has evolved, our framework stays the same. Begin with the macro. Find areas where forecasts are still reflecting overhangs from non-AI related headwinds and determine whether AI demand can overcome them in a way that makes estimates too low.

In this issue, we’re covering the following places that meet our criteria:

● Analog and Power Semis: Supply Chain Inheritance

● CPUs in the Agentic Era

● Neoclouds: The Inference Shortage

● AI Materials Bottlenecks

● Korea Unlocked

● Updating Previous Semis Memo Ideas

We end with Some Thoughts on Where We’re Going…

We first flagged the likelihood that AI demand would overwhelm the headwinds currently being experienced by the analog and power semi sector in our 25 Trades for 2025, specifically as it related to the upcoming Multilayer Ceramic Capacitors (MLCC) shortage.

Components integral to power quality management systems address common issues such as voltage sags, harmonics, and transients, thereby ensuring the reliable operation of electrical and electronic equipment. This includes capacitors, inductors, diodes, power ICs, surge protectors, filters, transformers, uninterruptible power supplies (UPS).

Discrete power semiconductors (like MOSFETs and diodes) will also benefit as they are integral to creating efficient, stable power rails. Filters, ferrite beads, and connectors may see growth, but the clearest secular uplift is likely in capacitors and inductors given their centrality to power conversion in AI-driven, high performance computing environments.

These names have begun to outperform, and we feel it’s directly related to another framework we’ve posed for 2026 – “Post-Traumatic Supply Disorder”. The companies dealing with power semis have had to contend with a barrage of headwinds – the COVID supply glut, competition from Chinese analog semis, the anemic EV and automotive cycle…the list goes on. However, they’re beginning to see data center revenues climb. And they’re not rushing to add capacity, having been burnt one too many times.

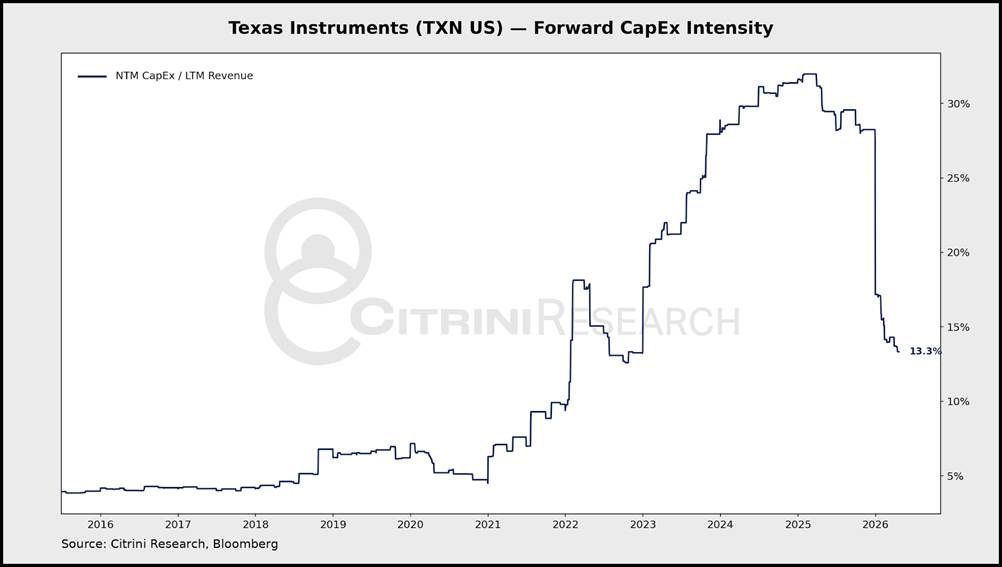

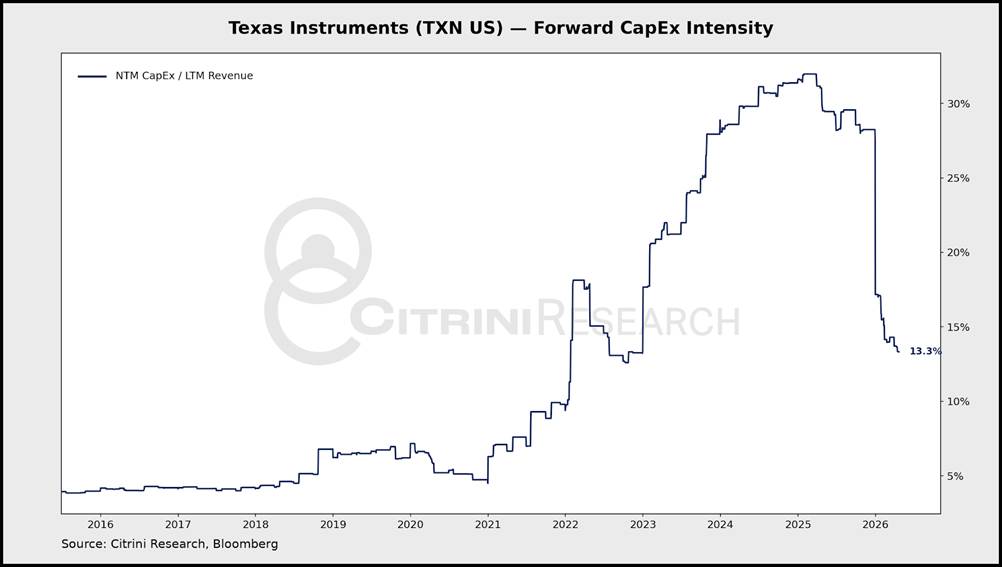

Take a look at the capex intensity (capex / revenue) for Texas Instruments (TXN US):

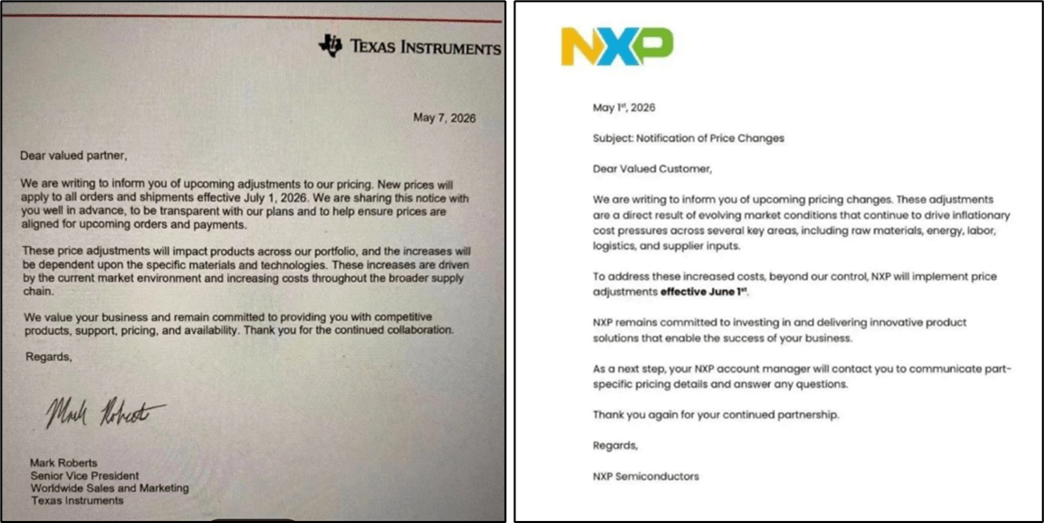

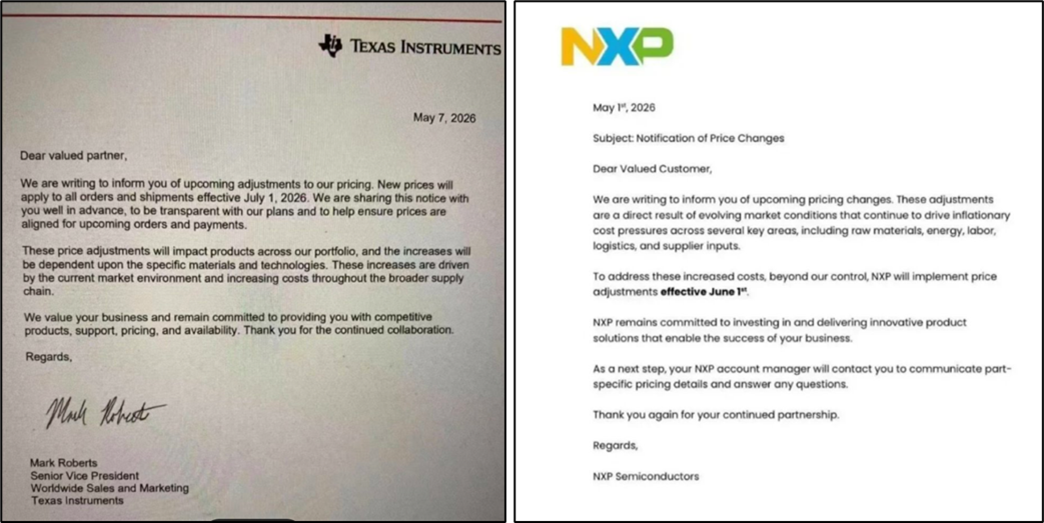

It’s typically this part of the cycle that results in supply ramping, but instead, TXN and peers like NXP Semiconductors (NXPI US)are content to raise prices.

Now, we’re at an inflection point, and these companies are letting ASPs go up rather than flood the market. Up until now, however, we’ve been mostly focused on the rack-internal story. Companies like Murata Manufacturing (6981 JP), Vishay Intertechnology (VSH US)and Samsung Electro-Mechanics (009150 KS)have taken off as the crowd recognizes exactly how short on MLCCs we are.

For our first and highest-conviction section, we’re glad to say that you don’t have to be a semiconductor expert to understand the rack-external power semis story. It’s a pretty cut and dry setup. The capex that burned them once was actually the exact infrastructure necessary for this part of the cycle.

While we’ve long been waiting for the automotive overhang to lift the fog off of the names in the analog and power semis space, we’re now realizing something more significant. It doesn’t really need to – rather, the AI capex buildout is simply inheriting the EV buildout supply chain.

In Nvidia’s May 2025 technical blog on 800V DC rack architecture, they credit the underlying technology to “the electric vehicle and solar industries.”That’s the trade…