**Innovation, Capital, and Deflation from First Principles

****by Allen Farrington and @sacha_meyers *

The central tenet of modern economic theology is that while too much inflation is a plague, too little of it is a catastrophe to be guarded against with every lever of macroeconomic intervention. What, exactly, counts as “too much” or “too little,” nobody can say. It remains one of the universe’s great mysteries.

The alleged perfect rate of inflation was not derived from a fundamental law of nature or from some sophisticated differential equation at the cutting edge of this highly rigorous and not at all pseudoscientific academic discipline. It was simply made up. As a Fortune article put it,

“The figure’s origin is a bit murky, but some reports suggest it simply came from a casual remark made by the New Zealand finance minister back in the late 1980s during a TV interview.”

With slightly more critical attention, Mises.org quotes the minister in question as later remarking that,

“The figure was plucked out the air to influence the public’s expectations.”

When pressed for a reason to fear a world in which things become cheaper, the fiat economist invokes the “Paradox of Thrift.” He argues that if a man expects a coat to be cheaper next year, he will choose to freeze today rather than part with his money. By this logic, saving is a terminal disease. The only way to keep a citizen “active” is to set fire to his savings through the quiet arson of inflation, forcing him to spend before his money goes up in smoke. To the fiat economist, deflation is the economy-killer, to be fought at all costs.

This essay is written to debunk that fallacy. In a society that values reality over accounting tricks, the number should go down. And if your money is honest, it will.

Good Deflation, Bad Deflation

“The products of the earth require long and difficult preparations in order to make them suitable for the wants of man.”

A.R.J .Turgot, Reflections on the Formation and Distribution of Wealth

We begin by rescuing the word “inflation.” To the state, inflation is a metaphysical abstraction, an exogenous act of God that simply happens to the economy. This is a convenient lie. We must distinguish sharply between cause and symptom. Monetary inflation is an act of the state: the deliberate expansion of the money supply. Price inflation is the consequence: the inevitable fever that follows the infection. By defining inflation solely as the “rise in prices,” the central banker shifts the blame from the printing press to consumer “expectations,” the “greedy” merchant, or the “disrupted” supply chain. Without a proper understanding of the cause, no solution is possible.

The fiat mind also relies on the myth of the “price level,” a statistical concoction that attempts to average the price of a haircut and a ton of steel into a single supposedly meaningful figure. What is the average temperature on Earth? What is the average length of a piece of string? The mind boggles.

There is no “general price,” only opportunity costs and individuals making choices based on their own subjective valuations across an unfathomable and ever-changing range of options. To claim that this aggregate can be managed through central planning is to suffer from a profound case of physics envy, despotism, or both. It is to treat a network of autonomous individuals as if they were gas particles in a sealed chamber.

No. Entrepreneurs act on intuition and anticipation of future conditions, not on the rigid “rationality” of a computer model. As the Nobel Prize-winning physicist Murray Gell-Mann remarked, “Think how hard physics would be if particles could think.” Indeed. Think how easy economics would be if people could not, and you will have the bulk of fiat economics.

This brings us to our core contention: long-term price deflation is not an exogenous malady emanating from vibey “sentiments.” It is an endogenous process of human progress. It is what happens when entrepreneurs—self-appointed and answerable only to their customers—risk capital to discover more efficient ways to marshal resources. When an entrepreneur successfully innovates, she offers superior, cheaper, or entirely novel products for a given investment. In other words, she frees up resources by consuming less to make more. “Less for more” is the heart of the flywheel: economic returns. Far from being a problem, this number going down is the force that drives economic progress. It is the steady mastery of nature and technique that converts a luxury into a necessity.

The fiat economist lives in perpetual dread of the “deflationary spiral.” Most popular discussions conflate two very different kinds of deflation. That distinction, and an account of the mechanics of each, is central to our argument.

Good deflation is when prices fall because entrepreneurs find ways to produce more or better output with the same input. Bad deflation is the fall in prices during a credit unwind. In that case, defaults rise, the credit binge ends, and everyone scrambles for liquidity. In such an environment, falling prices are a symptom of balance-sheet stress and broader institutional failure, not evidence that making things cheaper is destructive. Because bad deflation follows a credit unwind, fiat economists get the causality backwards. They conclude that printing money will avert hardship, not seeing that it was money printing that created the capital misallocation and balance-sheet fragility in the first place.

Good and bad deflation can be difficult to distinguish, but they are not the same animal. One is the dividend of competence; the other is the penance of hubris. Because the fiat economist cannot distinguish between them, he concludes that economic progress itself is a systemic danger. The “Paradox of Thrift” becomes the fear that progress might slow the engine down. And since that engine has already been corrupted by fiat thinking, it is imagined to be forever on the verge of collapse. So the consumer is coerced into action, told he must spend now because his money is a melting ice cube. The result is a frantic, hollow kind of prosperity: demand born not of genuine need, but of a desperate attempt to outrun the decline of the currency.

Two marginally more sophisticated variants of the fiat worry exist. One is that debt contracts are nominal, meaning that if prices and wages fall while debts stay fixed, the real debt burden rises. The result is a large wealth transfer to debt holders at the worst possible time. Another common refrain is that wages are sticky. Firms cannot or will not cut nominal wages quickly enough and instead lay people off. We agree that neither sounds especially pleasant. But notice what they imply. The central problem is not that prices fall because people can make things more efficiently, but that indebtedness and institutional rigidities are dangerous in a downturn. A society can vilify falling prices, or it can correctly identify the danger of building its entire economic system on fragile nominal promises. Choosing is left as an exercise for the reader.

The fiat economist universally chooses to set the printing press to brrrrrrrrrr. While the enlightened elite watch their stock portfolios moon and their debts disappear, the common man is told to be thankful that he was “this close” to the horror of living in a world where his wages bought more every year, and his government respected his private property. Imagine how hard it would be for that government to raise debt in such a world. It would have to justify its spending. We cannot have that.

Once we free ourselves from fiat methodology, we find that the only meaningful “stimulus” is the liberation of capital through innovation. With sound money and free markets, the number should go down.

The Temporal Logic of Pricing, Administration, and Technology

“All economic activity is carried out through time. Every individual economic process occupies a certain time, and all linkages between economic processes necessarily involve longer or shorter periods of time.”

F.A. Hayek, Money, Capital, and Fluctuations

Fiat economics treats time as inconvenient friction. In the hallowed halls of neoclassical theory, time does not exist. There is only “Equilibrium.” The market has achieved a Pareto-optimal stasis via the Walrasian auctioneer’s tâtonnement, yielding a price vector of zero aggregate excess demand. Every atomistic utility-maximizer has aligned his marginal rate of substitution with the price ratio, while firms reach a profit-maximizing zenith where marginal cost is perfectly aligned with marginal revenue. Perfection, as Michael Fassbender might say.

It is a beautiful but dead world. The “invisible hand” has stopped twitching, and all bow to the glorious General Equilibrium.

But if the equilibrium is absolute, why does anything ever happen? If all information is already “priced in,” how has anybody ever successfully invested? The answer is that the neoclassical model describes an idealized and hypothetical destination while ignoring the real and uncertain journey. It ignores the entrepreneur, the actor who operates not in a frozen, out-of-time model, but in the messy world unfolding at every instant. In assuming stasis, mainstream economics obscures the guiding light of entrepreneurs: returns.

Prices are set in time, not in equilibrium. Cash is spent today in the hope that uncertain cash flows will return to the entrepreneur and her investors later. That is a decent layman’s account of returns, and close enough for present purposes. Misunderstanding returns has serious consequences, because returns are the mechanism by which most real prices arise in the first place. By abstracting away time, neoclassical economics collapses a crucial dimension and blinds itself to a process at the heart of markets. It assumes firms maximizing profits when it should be looking at entrepreneurs experimenting to earn attractive returns.

To start with, we must recognize that prices are set by producers and accepted or rejected by consumers. So what is a producer trying to do when setting a price? The answer is simple: maximize long-term returns. In the real world, prices are discovered by entrepreneurs under uncertainty. Every worthwhile entrepreneurial venture is a bet on an unknown and unknowable future. There is no Walrasian auctioneer, only trial and error with the unforgiving feedback of profit and loss on investment.

This is because all production has costs, and in almost all circumstances, those costs come before any hope of revenue. Any productive enterprise therefore requires a base of capital rather than somehow operating, selling, and generating a return ex nihilo. Investment always precedes production, and production always precedes profit. Real resources are scarce, and real capital is scarce too. It follows that speculative opportunities to crystallize liquid capital into productive assets compete for sources of liquid capital—that is, money. Since money is homogeneous in this pre-crystallized state, its providers are not trying to maximize profits in the abstract, but profit per unit of committed liquid capital per unit of time: returns. Profit is a number. Returns are a relationship between money and time. An entrepreneur does not merely want to make money. She wants to make money relative to the capital committed.

We would encourage special attention to the dimension of returns: one over time. Whereas the dimension of profits is dollars, and the year-on-year increase in profits is a dimensionless ratio, returns are a true growth rate. Keep that in mind when a fiat economist tells you “the economy” “grew.”

Oh it grew, did it? It generated a positive return on reinvested capital?

Um … no … revenue went up.

That’s not “growth”.

Um …

Nice chatting with you as always.

Money is the economic stem cell. It is pure, undifferentiated potential. It is perfectly liquid and perfectly fungible. When you hold money, you are holding what can be thought of as a claim on the future output of the economic network in which the money is used. Investment is the process of crystallization and differentiation. When an entrepreneur "jumps off" the monetary network, they are differentiating stem cells into organs. They take liquid potential and freeze it into a specific, solid form: a bridge, a factory, or a decade of R&D for a life-saving drug. The more specific the organ, the riskier the crystallization and the higher the sought-after return.

As with seemingly every idea your humble authors have spent months or years pondering, it turns out Thomas Sowell captured its essence in two paragraphs from Basic Economics. Call it Sowell’s Law.

“A supermarket chain in a capitalist economy can be very successful charging prices that allow about a penny of clear profit on each dollar of sales. Because several cash registers are usually bringing in money simultaneously all day long in a big supermarket, those pennies can add up to a very substantial annual rate of return on the supermarket chain’s investment, while adding very little to what the customer pays. If the entire contents of a store get sold out in about two weeks, then that penny on a dollar becomes more like a quarter on the dollar over the course of a year, when that same dollar comes back to be reused 25 more times.”

And later, as a historical case study,

“One of the keys to the rise to dominance of the A & P grocery chain in the 1920s was a conscious decision by the company management to cut profit margins on sales, in order to increase the profit rate on investment. With the new and lower prices made possible by selling with lower profits per item, A & P was able to attract greatly increased numbers of customers, making far more total profit because of the increased volume of sales. Making a profit of only a few cents on the dollar on sales, but with the inventory turning over nearly 30 times a year, A & P’s profit rate on investment soared.”

It is worth lingering on time a little longer. Virtually no productive process is instant. All take time: the process of crystallizing money into productive assets takes time; the process of producing, bringing to market, selling, and recycling monetary gains takes time; and, most subtly but perhaps most importantly, recouping 100 percent of the capital committed usually takes a very long time and may never happen in full. Once crystallized as a productive asset, the goal is typically to operate the asset for years, not somehow both depreciate it 100 percent and return 100 percent. All such numbers are arbitrary in the abstract and set in practice by market forces, but a 5 percent nominal return requires 20 years just to recoup the initial investment, never mind to produce an economic return, assuming the assets generating that return even last that long.

One could argue that as the environment of accumulated capital grows deeper and more complex, the bar for competition rises with it, and entrepreneurs can only think in terms of returns rather than immediate profits if they hope to compete at all. They cannot compete without increasingly roundabout capital allocations, as Eugen von Böhm-Bawerk famously put it, and they cannot finance those allocations without long time horizons.

A simple entrepreneurial action might be a quick arbitrage. We see apples trading at different prices in two markets. We buy low and sell high. We crystallize our money into apples, walk them over to the next market, and sell them back into liquid money for a profit. We incur risk in the process—perhaps the price changes before we arrive—and it takes time. But the risk-adjusted return on the capital invested in apples, over the time required to complete the transaction, is worth it. Notice, too, that this action, driven by returns, affects prices. By moving cheaper apples into the expensive market, we narrow the spread. We should keep exploiting this money glitch until the two prices converge, once transportation and other costs are taken into account. That is the practical sense in which entrepreneurs are price messengers.

But simple arbitrage can only take us so far. Over time, entrepreneurs discover more organizationally complex and more intuitively speculative ways of satisfying people’s wants. This time, perhaps, we buy apples, turn them into pies, and sell those pies a few days later. That takes longer and requires capital equipment like an oven, which someone had to make. And someone had to build the factory that made the oven. And someone had to open the mine that produced the metal that made the oven that made the pie we are now selling. And everybody involved in all of this had to eat. Perhaps apples?

Think how deep the rabbit hole goes. Modern commercial society is built on astonishingly long and roundabout capital investments that can take years to pay off. And here, “paying off” simply means getting back on the money network of pure potential. A pharmaceutical company might spend 10 years on R&D and another 10 years selling the resulting product before it earns a satisfactory return on the initial investment. That is 20 years between jumping off the money network and getting back on. All this only to jump right off again in pursuit of another entrepreneurial journey. The roundaboutness of Dutch lithography giant ASML’s returns is barely comprehensible.

And so we see that “per unit of time” is just as important as “per unit of committed capital”: per unit of committed capital because money is homogeneous and liquid, whereas productive assets are heterogeneous and illiquid; per unit of time because the process of transformation not only takes time but commits the capital provider to an extended period of heterogeneous exposure. To reiterate, then, producers care about profit per unit of committed capital per unit of time: returns.

So we ask once again: what does a producer decide with respect to prices in order to maximize returns? There are several candidate answers, all in tension. There is no single “correct” answer. Balancing what follows is the essence of entrepreneurship: intuiting future consumer behavior and future market conditions.

Keeping in mind that producers are almost always in some degree of competition with others selling similar, if not identical, goods or services, there is always a temptation to lower prices and draw customers away from rivals. Obviously, this can harm returns, so prices cannot be lowered to zero. But equally, while returns can on paper be pushed arbitrarily high by raising prices, that assumes the same quantity of sales. It will not be. Higher prices mean fewer sales as consumers go to competitors instead. Exactly how many fewer is the essence of entrepreneurial judgment. Contrary to fiat economist logic, there is no such actual thing as a demand curve sitting out there in the world. There is only the producer’s intuition about how consumers will respond.

There is a subtle but critical distinction between the fact that some best possible outcome exists and the claim that anyone can deduce how to achieve it. Armen Alchian put the point well in Uncertainty, Evolution, and Economic Theory: “the meaningfulness of "maximum profits" as a realized outcome is "perfectly consistent with the meaninglessness of 'profit maximization' as a criterion for selecting among alternative lines of action."

Consider a baker deciding how to price a new loaf. She could charge £3 and sell 200 a day, or £4 and sell 100, or £2.50 and sell 300, but exhaust her staff. One of these paths, or perhaps some option she hasn't considered, would yield the highest return on her capital. That optimum exists in principle. But she cannot calculate her way to it because the outcome depends on the subjective preferences of hundreds of people she has never met, the pricing decisions of competitors she cannot observe in real time, and much more besides. She can only try something, watch what happens, and adjust. This is not a failure of her rationality. It is the nature of the problem.

Fiat economists, seduced by the quantifiability of profit, mistake the existence of a theoretical maximum for the existence of a method to find it. They then build models that assume the method has already been applied and wonder why reality keeps misbehaving.

There is also, once again, the component of time. The producer cannot sit around indefinitely waiting to discover the perfect price. Even if that were possible—which it is not—by the time she found it, it would already be wrong. To return to the physical dynamics of returns, if in Scenario A we sell our widget for $x, and in Scenario B we sit around pontificating about the “perfect price” only to sell it later for the same $x, our returns in Scenario A are by definition higher. Time is valuable, not as a hand-wavy slogan, but in a very real and fundamental sense.

The production process increasingly crystallizes value into more definite forms, culminating in inventory waiting to be sold. The producer, therefore, has some desired period over which sales should occur so that liquid capital can be recycled into the production process.

With that in mind, we can give our first concrete answer. Relative to whatever time period is desired, if inventory is selling too slowly, the producer should lower prices to move it faster. If inventory is selling too quickly, the producer should raise prices to capture more immediate profit. The latter is a good problem to have, but it is still a problem from the standpoint of inadequately maximized returns. In either case, the producer is responding to what she believes are market signals: if sales are too slow, perhaps a competitor has a lower price and consumers are going there; if sales are too fast, perhaps the market is not yet saturated and higher prices will improve returns without slowing throughput beyond the producer’s desired cycle.

Note that, in either case, the producer is both responding to market signals and creating them. Lower prices may reduce returns across the market and push marginal capital into other industries. Higher returns, conversely, attract capital here. All entrepreneurial decision-making is, in the end, capital seeking returns, even when it presents itself in some more concrete form several degrees removed.

The entrepreneurial process just described has a fortunate long-term consequence: innovation. In the short term, entrepreneurs decide how to price inventory that has already been produced but not yet sold. That is all the consumer directly sees, and from the entrepreneur’s perspective, it is the immediate point of the exercise. But productive assets exist on a spectrum of heterogeneity and liquidity, and over horizons longer than the ideal stock-turn window, the producer faces a different question: what actually drives returns? In the broadest terms, the answer is creating more output with the same inputs. Competitive pressure at the point of sale makes that unavoidable wherever competition exists at all.

To make that more concrete, a producer hoping to maximize returns—whether by increasing them in the absence of competition or preserving them under competition—has only three broad options: create products and cycle inventory faster, raise prices, or lower costs. “Create products and cycle inventory faster” is really another way of saying “sell more,” but with the emphasis on time rather than quantity: selling the same amount in a shorter period is functionally equivalent to selling more in a fixed period. Most strategies are combinations of these three.

The simplest option is that if returns are already attractive enough, the producer can allocate more capital to the same enterprise. This need not require faster turnover, higher prices, or lower costs. It may counterfactually simply reflect the absence of enough pressure to force any of those changes. The opportunity appears to be there. Competitors do not seem to be taking it. She may as well take it herself.

Sales and marketing can be understood as attempts to cycle inventory faster, raise prices, or both. Marketing may broaden the market by making potential customers aware of a product they would otherwise have ignored, thereby increasing sales over a given period. Or it may aim to create a perception of quality that allows the producer to raise prices—or, counterfactually, not to cut them when otherwise she would have had to.

R&D is typically aimed either at lowering costs by discovering cheaper ways to operate productive assets or at creating better or entirely new products. That serves to lower costs, sell more product, or cycle inventory faster.

Everything described so far in this section can be subsumed under “investment” or, if the reader prefers a more elevated phrase, “capital accumulation.” Returns are maximized by investing in innovation, either by opening new markets or creating new products.

Note, too, that investing is necessarily speculative. Expanding production by allocating more capital to the same assets assumes that a larger market exists at the same return-generating prices and that competitors will not chase those returns hard enough to drive them below whatever rate is deemed attractive. Sales, marketing, and brand-building are likewise uncertain. They may work; they may not. You can have a hunch, but you cannot know until you try—and even then, you may not really know. R&D is even more obviously experimental. It makes no sense to speak of “just discovering new or better products” or “just making things cheaper” as though these outcomes were sitting on a shelf waiting to be collected. You cannot know they will work until you try, but neither do you try at random. The effort follows from an informed hunch about technology and administration. With only slight overgeneralization, long-run cost declines are almost always the product of new technology or new methods of business administration, or both.

This tacit knowledge is arguably the entire crux of entrepreneurship: it cannot be known in the abstract, or centrally, or macroscopically. It cannot even be articulated macroscopically, never mind discovered. Nor can it be guessed or arrived at by a random walk through concept space. Nor can it be hit upon by investing in absolutely everything because resources and hence capital are scarce. Entrepreneurs intelligently and pro-socially allocating capital in search of returns drive all production and hence all wealth creation.

This iterative process is little more than another way of describing price discovery. Every day, entrepreneurs discover how many goods can be made, what they can be sold for, and whether that justifies the capital outlay. This activity is radically uncertain, as Frank Knight defined it in his 1921 book Risk, Uncertainty, and Profit:

“Uncertainty must be taken in a sense radically distinct from the familiar notion of Risk, from which it has never been properly separated. [...] It will appear that a measurable uncertainty, or "risk" proper [...] is so far different from an unmeasurable one that it is not in effect an uncertainty at all.”

There is no base rate when inventing something genuinely new. These are acts of creation, just as almost every economic action is, since we never step into the same river twice. Of course, not all price discovery is equally uncertain. When you buy ice cream at the supermarket because you think you might enjoy it later that week, you are taking a tiny bet about the future. You may change your mind and decide it is time for a diet, but the stakes are low. When Elon Musk risks bankruptcy to disrupt the economics of space travel, we witness extreme price discovery in extreme form, which is why it is rewarded so extravagantly.

Dynamic Capital Allocation

“The concept of production as a process in time … is not specifically “Austrian.” It is just the same concept as underlies the work of the British classical economists, and it is indeed older still – older by far than Adam Smith. It is the typical businessman’s viewpoint, nowadays the accountant’s viewpoint, in the old days the merchant’s viewpoint.”

John Hicks, Capital and Time

So far, so sensible. Entrepreneurs try to maximize returns under competitive pressure on prices in the short term and under competitive pressure to innovate in the long term. So what, exactly, are the fiat economists supposed to object to? At first glance: not much.

But this is where we hit the first fork in the road. The mainstream economist will insist that if this process of innovation-driven price declines becomes generally understood, people will simply wait for things to get better before they consume. Aggregate demand will fall, and all hell will supposedly break loose.

Consider the supposed problem in the abstract. If you are hungry, and you know apples will be 2 percent cheaper next year, will you wait a year? Of course not, because you would die, and you would prefer not to die. There is nothing irrational about that. We can broaden beyond such a dramatic example: would you ever delay a purchase because you knew it was going to be cheaper? Here, the matter becomes more interesting. For some things, perhaps you would. We need not pretend nobody ever delays discretionary consumption.

Or, put differently, there is a sliver of truth in the so-called Paradox of Thrift: nobody’s time preference is zero. You cannot only produce and never consume. You need to eat, to be clothed, to have shelter, and so on up Maslow’s hierarchy as relative abundance allows.

To illustrate this, let us entertain the Keynesian nightmare of a society that delays all but absolutely essential consumption. Such a society would have plenty of capital for reinvestment. Instead of eating the seed of its labor, it would plant the seed. But why, if it will not eat the next harvest either? To plant it again. And it does not take long, once one plays with a compounding table, to see that even the sternest apostles of delayed gratification will eventually accumulate so much capital that their Aurelian stoicism will crack. And if it did not, the society would continue compounding its technology and productive capacity at an astonishing rate. Were it ever to stop or even slow down, cash would come gushing out, much as it would from a company that had spent decades reinvesting everything into growth. The real question, then, is not “consume or never consume,” but “what do we consume now, and what do we invest so as to consume later?”

There are trade-offs here grounded in uncertainty and subjective valuation that cannot be quantified, only intuited. So yes, entrepreneurs react to present consumption patterns when hypothesizing future consumption patterns and deciding how to allocate capital. But to jump from that obvious observation to the claim that “investment is a function of current consumption” is ridiculous.

We often hear fiat economists decry “hoarding,” but what they usually mean is that people are saving and investing. With more hoarding, perhaps we would build fewer automobiles, but more machines that build automobiles. And if people became especially thrifty, the economy would climb higher up the stack still to build the machines that build the machines that build automobiles. The thriftier we are, the more roundabout our production methods become and the deeper our capital base grows. Such a society would be living for a better tomorrow.

Let us also get one thing clear. Even if people quite literally stuffed money under the mattress, that would still benefit society. Holding money for longer simply means elongating the average holding period of money. People are storing more of their labor in the monetary system. That raises the value of money relative to goods and services and therefore lowers prices for everyone else. Under a hard monetary system, people are rewarded for participating in the system. By holding monetary capital and operating on that network, they give it depth and liquidity, thereby empowering entrepreneurs on that same network to try to make things cheaper. A worker whose savings sit on such a system helps underwrite innovation and then benefits from the resulting deflation. She did not receive that benefit for doing nothing. Her reward came from backing a monetary network that fosters innovation. In none of these scenarios is capital “wasted.” Yet the people most worried about the evils of delayed consumption will tell you that deliberately destroying useful assets is a net good.

Before we trick ourselves into thinking deflation will cause more deflation until everybody starves, we must recognize a distinction the fiat analysis elides. Producers are in constant competition with one another. Consumers are not. Consumers deciding to delay a purchase face only opportunity costs. Their consumption satisfies only their own subjective values.

Producers, by contrast, are in a different position altogether. They are always competing against other producers on price in the short term and on innovation in the long term. Emphasizing that competition is against real rather than hypothetical competitors, that it generates real rather than hypothetical returns, and that it relies on tacit rather than “perfect” knowledge, Alchian writes,

“Realized positive profits, not maximum profits, are the mark of success and viability. It does not matter through what process of reasoning or motivation such success was achieved. The fact of its accomplishment is sufficient. This is the criterion by which the economic system selects survivors: those who realize positive profits are the survivors; those who suffer losses disappear. The pertinent requirement – positive profits through relative efficiency – is weaker than “maximized profits,” with which, unfortunately, it has been confused. Positive profits accrue to those who are better than their actual competitors, even if the participants are ignorant, intelligent, skillful, etc. the crucial element is one’s aggregate position relative to actual competitors, not some hypothetically perfect competitors.”

The analysis changes quite fundamentally once we consider price declines in capital goods, which necessarily precede price declines in consumer goods for the reasons already discussed. A producer cannot simply wait around to earn a higher return later by allowing her own costs to fall in the meantime, because capital accumulation is iterative and competitors can always iterate faster. If the price of some key capital good is falling because its producers have invested successfully in pursuit of returns, you could postpone buying it in hopes of an even better entry point later. But you are probably better off buying it now, lowering your own prices, increasing your own returns, and putting yourself in a stronger position to buy again later from a better-capitalized base. The alternative is to sit still while your competitor buys the cheaper capital good first, cuts prices, takes your customers, crushes your returns, and leaves you without the money to buy anything later at all.

Once again we encounter the failure of static analysis. If you somehow knew you had no competition and could afford to wait for lower costs in the future, then yes, you might imagine boosting returns this way. But even that collapses on inspection. If you have no competitors, who is buying the capital goods in question? If nobody is, how is the producer of those capital goods earning the returns required to fund the R&D that is causing the deflation in the first place? The circle cannot be squared. No circle can. Non-zero consumption creates the price signals that direct capital allocation, not merely at the level of consumer goods, but at every level of capital goods that underlies productivity and wealth creation in any remotely complex economy. To the extent demand is ever truly stimulated, if it is real and sustainable, it is stimulated by deflation.

Competition has another helpful consequence: it bids up the price of labor and other inputs. Entrepreneurs would certainly like to pay workers less, but in a competitive market, workers can play employers against one another and demand the highest wage that still makes economic sense. That wage is linked to their productivity, which is itself increased by access to better tools. The more tangible and intangible capital workers have available to them, the greater their bargaining power and the higher their wages. So not only do entrepreneurs make things cheaper for consumers, they also help workers earn more. Once again, the fiat fear confuses the effects of bad deflation on wages during a credit crunch with the effects of good deflation produced by rising productivity. A worker does not need nominal numbers to rise to be better off. He needs purchasing power to rise.

Switching now to consumers, it is undeniable that they can delay discretionary purchases if they wish. But they must consume something to survive, and that fact alone gives entrepreneurs a clear signal to focus on necessities and bring their costs down as far and as fast as possible. Under a hard monetary system, entrepreneurs are pushed toward making essentials cheaper, not merely toward selling luxuries. And “essential” here is not defined by some committee, but pragmatically by what people actually choose to spend on in a world where their money is not being set afire by enlightened elites “stimulating” the economy.

Consumers are also often producers. In that capacity, they compete with other producers and must spend to remain competitive. A worker may buy an automobile because it gets him to work faster or more comfortably than the bus. That is consumption, certainly, but it is also productive consumption. It channels resources toward goods and services that genuinely augment the economy’s productive potential.

The perverse reality under fiat is that monetary inflation kills the incentive to save and reinvest. People are nudged toward spending more on luxuries—a PlayStation, a package holiday—and less on productive reinvestment. In a system free of monetary lies injected from above, people would consume what they truly wanted and invest the rest into improving the economy. So yes, luxuries would probably see lower demand if the printer stopped. Good. That would come at the gain of better alternatives, a fact that only becomes visible when prices are allowed to transmit information clearly. Entrepreneurs would quickly reallocate capital. We would probably get fewer Ferraris and more life-saving drugs.

The fiat economists want to have their cake and eat it too. There are essentially no entrepreneurs in their static models. Nobody prices anything; things simply have prices. Nobody makes plans; things are merely produced and consumed. Firms are imagined to “maximize profits,” and if prices do not keep rising their incentives supposedly break and the machine stops.

Charlie Munger had an amusing quip attesting to the dynamics at play here:

“When we were in the textile business, one day, the people came to Warren and said, “They’ve invented a new loom that we think will do twice as much work as our old ones.” And Warren said, “Gee, I hope this doesn’t work because if it does, I’m going to close the mill.”

He knew that the huge productivity increases that would come from a better machine introduced into the production of a commodity product would all go to the benefit of the buyers of the textiles. Nothing was going to stick to our ribs as owners.

And it isn’t that the machines weren’t better. It’s just that the savings didn’t go to you. The cost reductions came through all right. But the benefit of the cost reductions didn’t go to the guy who bought the equipment. It’s such a simple idea. It’s so basic. And yet it’s so often forgotten.”

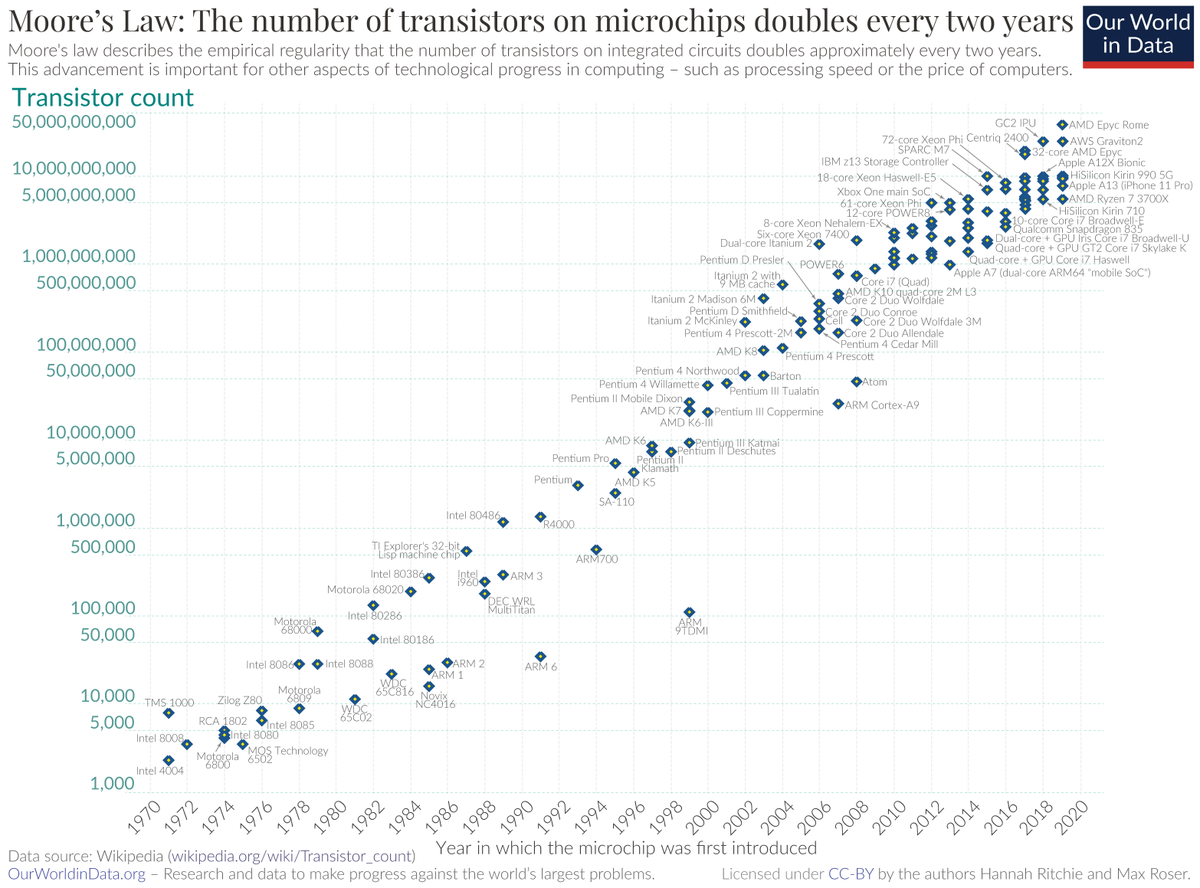

Buffett understood how much more would have to be spent to keep selling into a market where the product was relentlessly becoming cheaper. That calculation simply was not attractive enough, so the money went elsewhere. The same logic holds across industries with capital goods or long-duration intangible investment—which is to say, across almost every serious industry. But we can end the section with a more accessible example: Moore’s Law.

In case the reader is unaware, Moore’s Law—not a real law, merely an impressively accurate long-standing prediction—holds that the price of computing power roughly halves every 18 to 24 months. Much less well known, but more important here, is that Moore’s Law is really a special case of Wright’s Law, which says that in any production process, costs tend to fall by some stable amount for each increase in cumulative historic production. Semiconductors simply happen to exhibit this dynamic at extraordinary speed, and have done so for so long that Moore’s Law can be expressed as unfolding over time.

Emphasis on: unfolding over time.

If it were even remotely true that people defer consumption merely because deflation offers a better entry point later, then Moore’s Law would imply that nobody has ever bought a computer or invested in producing one.

Were the fiat thesis correct, anyone who wanted to compute something in 1970 would still be waiting for this terrible deflation to stop. Of course, the opposite is what actually happened. Computers are extraordinarily valuable capital goods. They help entrepreneurs innovate better, cheaper, and entirely new ways of producing almost everything else. So entrepreneurs have aggressively bought them, justifying the purchases on the back of returns, which in turn allowed the producers of computing hardware to earn healthy enough returns to reinvest. Cumulative production exploded, and prices collapsed. Nobody starved. Quite the opposite: countless lives were almost certainly improved, and many saved, as a downstream consequence.

It is also worth noting that this is the fastest and most durable Wright’s Law coefficient of which we are aware. Virtually every other technology in which capital can be invested in pursuit of returns deflates more slowly than semiconductors do. It is therefore even less sensible to imagine people deferring purchases indefinitely merely because prices are likely to be lower later.

The proper interpretation of the so-called Paradox of Thrift is that it reveals the fear that fiat economists live under: that people may stop consuming luxury products they could never really afford, products they were tricked into consuming by inflationary lies. They cannot tolerate a world in which people are allowed to discover for themselves how best to allocate their finite resources.

This fiat worry is not merely sloppy thinking; it is a negation of history. Great capitalist fortunes are almost always amassed by drastically lowering prices for consumers. To the fiat Paradox of Thrift, we oppose the empirical Jevons' Paradox—also not really a paradox, but we do not name these things—which states that as technology or efficiency lowers the relative cost of a resource, new uses of that resource become profitable, and total demand rises. The resource becomes cheaper, yet more is spent using it, not less.

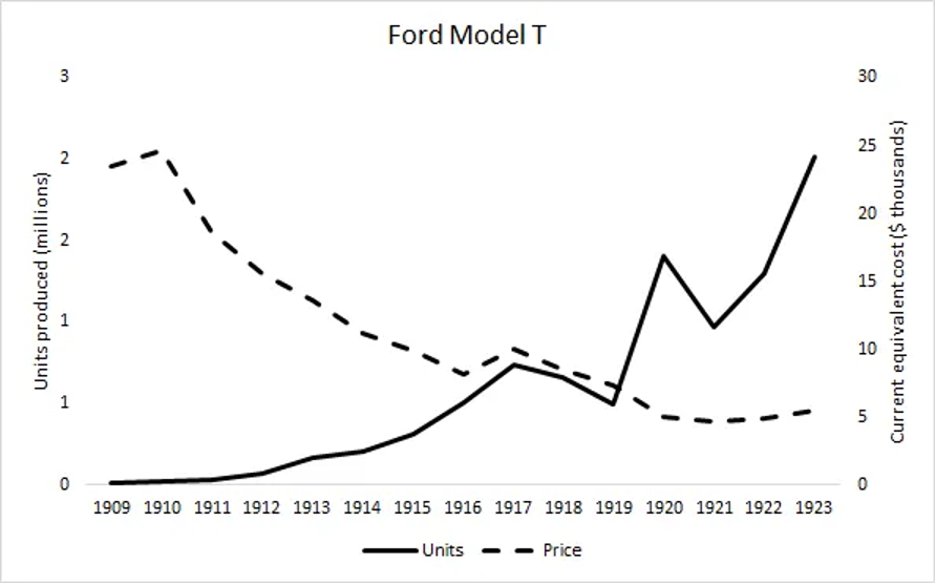

Carnegie made his fortune by lowering the cost of steel. Vanderbilt used increasingly affordable coal, steam engines, and steel to build railways that lowered transportation costs and opened up markets. Rockefeller relentlessly expanded the use of oil by innovating and passing cost savings through to consumers. Henry Ford pushed the logic to its natural conclusion. His policy was “to reduce the price, extend the operations, and improve the article,” thereby enlarging the market and generating profits that could immediately be reinvested in making the automobile cheaper still. As Ford said,

"Profits made out of the distress of the people are always much smaller than profits made out of the most lavish service of the people at the lowest prices that competent management can make possible."

The empirical result of his actions speaks for itself:

The Effect on Prices

“Economic medicine that was previously meted out by the cupful has recently been dispensed by the barrel. These once unthinkable dosages will almost certainly bring on unwelcome after-effects. Their precise nature is anyone's guess, though one likely consequence is an onslaught of inflation.”

Warren Buffett, 2011 Letter to Berkshire Hathaway Shareholders

So far, we have considered only individual decision-making by entrepreneurs. That is methodologically sound, since only individuals make decisions. But having been careful on that front, we can still ask what emergent patterns we should expect from these individual decisions about capital allocation, pricing, and innovation. Several conclusions follow.

At the level of the individual producer, there is always pressure to increase returns lest the avenue of investment cease to attract capital. In the short term, this may mean raising prices or lowering them, perhaps counterintuitively. Which response is right depends on the demand perceived relative to the supply made possible by the existing stock of productive assets. The answer cannot be derived and is, in principle, unknowable; it can only be intuited.

In the long run, however, it is reasonable to expect returns to tend toward equalization as competition directs liquid capital toward its most promising illiquid forms. That is very different from saying the process is automatic, immediate, and smooth or that it ever concludes. Capital allocation is uncertain, iterative, temporal, and intuitive. The “pressure” here is not a natural law like fluid levels equalizing or temperature gradients dissipating. It is only a reasonable expectation about what human beings with money and incentives will tend to do. Economic forces may push in a given direction, but in a dynamic adaptive system, they never produce a true equilibrium. At most, equilibrium names an expected tendency given current knowledge and incentives. And even that can be understood only counterfactually, not modeled directly. The only way to acquire the knowledge in question is to run the experiment that creates the facts one wants to know.

The pressure to increase returns—and, under competition, to preserve an acceptable return—can only be satisfied in the long run by investment: by experimentally discovering new knowledge that makes it possible to create more with less, better with the same, or something entirely new.

Because this logic is agnostic as to the specific avenue of capital allocation, and because liquid capital is fungible across industries, we can say in the aggregate: prices go down only where investment has created a new support level for returns such that producers can lower prices, take market share, and still increase returns. Producers can always cut prices in theory, of course, but without a sufficiently improved cost base, they risk lowering returns rather than raising them. Once investment has genuinely lowered the cost structure, however, price cuts become far more likely to increase returns than to destroy them. Prices, therefore, do not mysteriously “go down.” The price level is not an exogenous parameter. It emerges from individual decision-making under uncertainty, from the drive to maximize returns on capital, and from the possibility of discovering more efficient methods of production.

It is also important to note that when any individual producer lowers prices in this way, everyone else’s real returns rise as well. The effect will be unevenly distributed across time and economic distance, but the ripples spread outward. Every unit produced by somebody is consumed by somebody else. That is what exchange is. So when a producer innovates and lowers prices to take market share and increase returns, she is also lowering other people’s costs and thereby increasing their real returns.

The fiat mindset encourages people to imagine that lower prices mean less economic activity. This is a silly result of static analysis. Lower prices are only possible because either more output is being produced with the same inputs or the same output is being produced with fewer inputs. This takes us back to Jevons. The mainstream explanation is simpler than the framework discussed in this essay, but it captures something real: when things become cheaper, they are used more, not less, because new applications become economically viable. Although it may seem intuitive, to fully understand the phenomenon, we need the machinery developed throughout this essay: innovation in pursuit of returns, producers lowering prices to capitalize on improved cost structures, and the downstream gains others enjoy from the resulting reduction in costs.

We can state the same point more abstractly. The aggregate result of this process is the continuous accumulation of more and better tools—a perfectly respectable definition of capital, provided we understand “tool” broadly enough to include not only the spade but the idea of the spade and the skill required to use it. The more tools society has, the more valuable everyone’s time becomes, because it can be leveraged to create more, better, and newer outputs with the same raw input of hours. Innovation and capital accumulation mean that everyone’s time is becoming more valuable.

This framing also reminds us that the whole dynamic depends on consumption being sustainable. Nobody’s time preference is zero, and returns require profit. Investment can be funded by savings, but savings cannot be drawn down forever. Savings exist only where positive returns are not wholly consumed. So there is always a balance between what is consumed and what is saved. If we only consume, we never invest, and productive assets depreciate away. If we only save and never consume—not even necessities—then producers have no signal as to what should be produced and consumers starve. Anything short of universal self-starvation kicks the reinvestment engine into motion and improves living standards through deflation.

These absurd extremes illuminate the tension within which a balance is discovered. And it is here that interest rates emerge. The question faced by any would-be investor is always: at what price am I satisfied abstaining from consumption with some portion of my savings? The “price” in question can only mean an amount of money per unit of committed capital per unit of time. That definition describes both returns but also interest, which is merely rate of return. To the entrepreneur, any given interest rate or return is justified only relative to an expected rate of return.

If savings are flowing heavily into present consumption rather than investment, then returns on satisfying that consumptive demand are likely high, and marginal consumers will be tempted to become investors instead. If savings are flowing heavily into investment rather than consumption, then returns will tend to be lower, and marginal investors will be tempted to consume instead. That is the balancing process.

It is also amusing to note that the deflationary mechanism just outlined “stimulates consumption” in a healthy way, because even when people know something will be cheaper later, there is always some price at which they crack and buy it now. As prices fall, demand materializes. But it does so through real price signals rather than by forcing people to spend before the state kills the value of their money.

While the logic of this dynamic can be understood, it resists quantification. It is not “scientific” because no controlled experiment can isolate one variable from all the others. The experiment is always counterfactual until it is run in reality, and running it is precisely what generates the knowledge sought. Nor can the aggregate be treated as unitary. It is and can only be emergent. To the extent it meaningfully exists, it exists only as the product of individual, marginal decisions. The idea that some authority can deduce the correct level of this balance is not merely wrong; it is not even wrong. It is methodologically incoherent. Asking for the “correct interest rate” is like asking how much the color orange weighs.

**

Money**

“A new car, caviar, four-star daydream

Think I'll buy me a football team.”

Pink Floyd

We deliberately left money to the very end. The essay has first tried to show that price deflation, understood as a broad tendency for goods to become cheaper over time, is a natural consequence of free capital markets and the possibility of discovering new technologies and better methods of administration. One might go further and say that price deflation is not merely a consequence of progress but a definition of it. Economic activity that does not make things more affordable is change, but not progress. So let us conclude by asking what different monetary regimes do to this process.

Once money enters the picture explicitly, we must be careful to distinguish between the “price level” and the “money supply.” A first confusion to clear away is that while there is such a thing as inflationary money, whose supply can be expanded, there is not really such a thing as “deflationary money”. One could imagine a money whose issuer periodically destroyed units or reduced balances programmatically, but we know of no relevant real-world example.

This is perhaps the point of maximum confusion for fiat economists, who tend to make a partly theoretical and partly practical argument along the following lines: in an inflationary fiat system, where almost all money is really bank credit, bad loans impair creditors’ solvency, so creditors call in other loans to recapitalize. Because a prior credit bubble has spread far more debt through the financial system than real savings ever justified, the process becomes self-reinforcing. Everyone scrambles to recapitalize with real assets. Loans go bad and are called in at the same time. Investment funding dries up. Consumption dries up too, because everyone realizes they have far less genuine savings than they thought. New credit extension dries up as well. Since credit extension is treated as synonymous with money, this is often framed as the money supply itself contracting. Producers, faced with retrenching consumption, then slash prices to clear inventory. That is the beginning of bad deflation. One might call it a deflationary credit spiral. What matters is that this has nothing whatsoever to do with innovation-driven deflation.

We are now talking about something much murkier than entrepreneurs finding cheaper ways to satisfy consumers. We are talking about the demand for money. Like innovation, it is endogenous and bottom-up. Unlike innovation, it is purely monetary. And because “demand for money” is among the most abused phrases in fiat economics, we should be very clear: read it not as “desire for credit,” but literally.

Demand for money is a person’s subjective desire to hold a given amount of wealth in liquid monetary form at the implicit opportunity cost of buying anything else. People with a high demand for money will exchange goods, services, and investments for money because they value its liquidity and its usefulness as a store of value and medium of exchange. Jews fleeing German persecution during the Second World War had little use for illiquid goods or local hard assets. They wanted portable, liquid money, which often meant gold. Conversely, someone with no heir and terminal cancer may have little demand for money, because he would rather spend everything before he dies.

When demand for money rises, perhaps because of war or fear, people “cash out” and we observe a purely monetary and endogenous form of deflation. Another way of saying the same thing is that the price of money has risen relative to other goods and services. Demand for money at the previous price exceeded supply, so the price of money rose. From the perspective of someone using the currency as a unit of account, that looks like a general fall in prices. The monetary network is now storing more value while the stock of goods and services has not changed. This is precisely the kind of deflation Keynesians fear, because their entire worldview assumes people should be induced to get rid of money as quickly as possible. Their pyromania aims to lower the demand for money and thereby create price inflation.

To bring some balance to the matter, it is true that a sharp increase in the demand for money is often a worrying sign, such as during a credit crunch, when people are no longer satisfied with IOUs from lenders or from their own fractional-reserve bank. They want cash instead. Claims that had previously circulated through the system with almost no one holding base money for long are suddenly called into question. That unwinding causes real pain. But the correct analysis is that the pain is necessary because the problem is real. The credit expansion reverses only because it was unsound.

Credit collapses are painful, but to identify the temporary price declines associated with them as the root problem is absurd. That is like saying that because hangovers are unpleasant, sobriety must be the cause, and the solution must therefore be to keep drinking. The actual solution is not to get drunk in the first place, or, failing that, to sober up. Fiat economists have a habit of responding to every crisis with the same recommendation: just one more drink. Instead of reckoning with malinvestments and accepting that people’s demand for money has genuinely increased, Keynesians refuse to let nominal prices drop. Since the average holding period of money has elongated and caused monetary deflation, the only solution is to expand the quantity of money.

In a fiat-credit system, money is not merely the base currency. It is a towering structure of promises layered on top of it, such as bank deposits. In the boom, those claims multiply. In the bust, they evaporate. If one wants fewer deflationary spirals of this kind, the answer is not to print more. It is to build less of civilization on fragile, maturity-mismatched nominal claims backed only by other liabilities rather than by real assets. Yet the standard policy response is to treat the collapse as proof that prices must always rise, and to justify permanent monetary debasement in order to prevent the next collapse, thereby laying the groundwork for a still larger one.

Economic collapse may not even be the worst consequence of fiat managerialism. Setting morality aside, inflation has two technical effects: it breaks price signals, and it redistributes purchasing power. Prices are how human beings coordinate across time and space under uncertainty. They tell entrepreneurs and consumers what is scarce, what is abundant, and where capital may earn an attractive return. Within this family of prices sits the interest rate, which is not a dial the FOMC can turn at its regular meetings to achieve full employment. It is the price of the present against the future: the terms on which savers defer consumption and entrepreneurs invest. It is the manifestation of time preference, risk, and opportunity. It is an information signal.

New money never arrives everywhere at once. It enters through particular channels and benefits those closest to the spigot at the expense of those furthest away. Banks, governments, and asset holders cluster near the source. “Stimulus” becomes synonymous with financialization, leverage, and the migration of talent toward politically connected activities. If you pay people for proximity to the printer, do not act surprised when fewer of them build bridges.

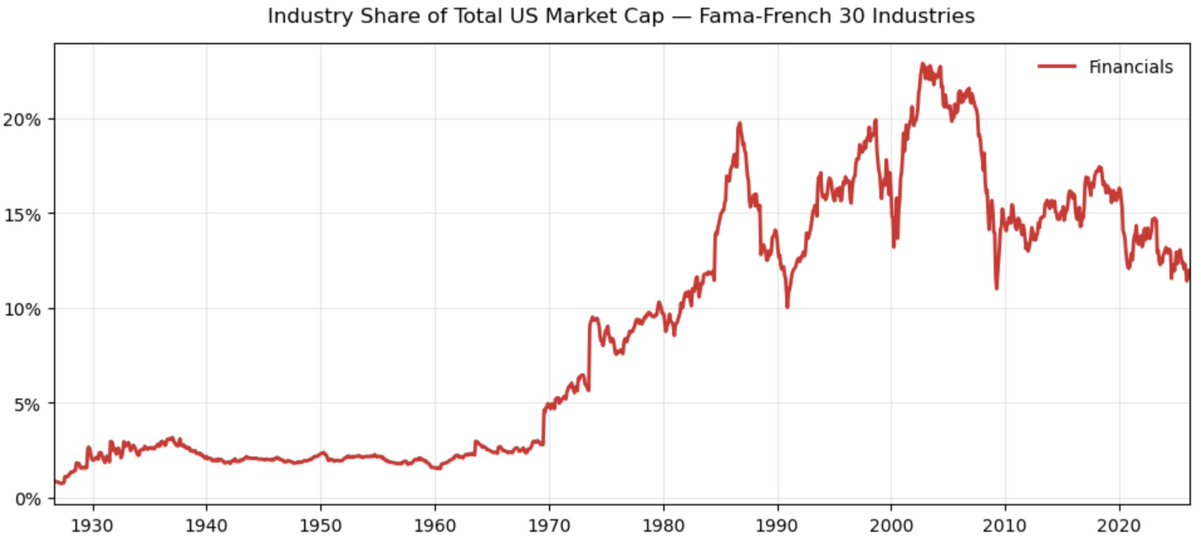

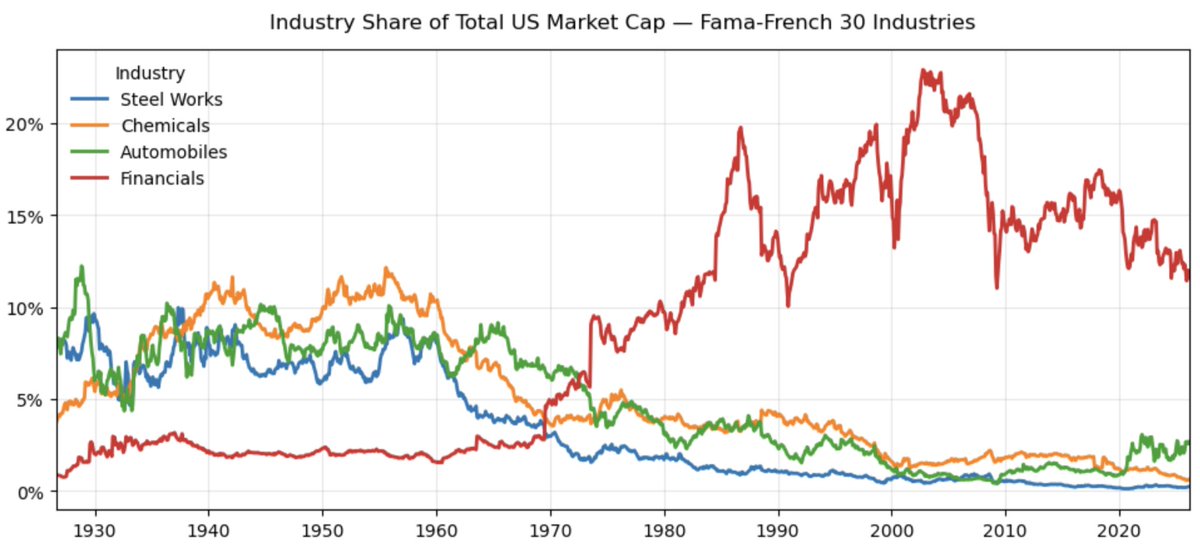

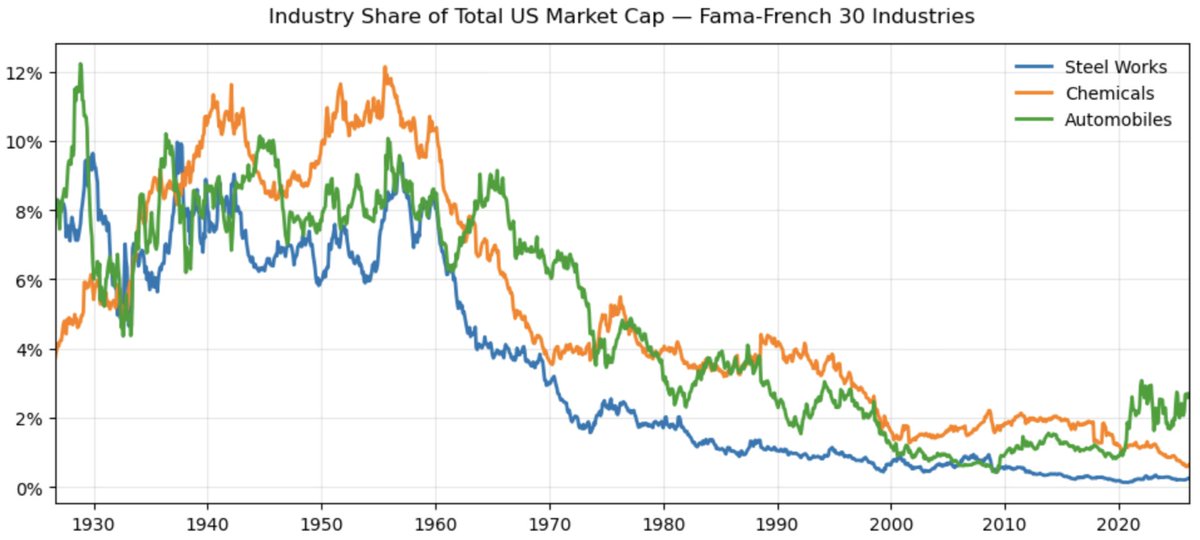

We can visualize both this Cantillon inflation and technologically driven deflation at the same time in the composition of stock market indices. By considering a period of time that captures both the ultra long term compounding effect of technological innovation and which overlaps with critical monetary shifts, we get a crude sense of what is getting cheaper and what is getting more expensive. Consider the absolutely critical industries of steel, chemicals, and automobiles. Once major components of the US index, we see the relentless drive of innovation and deflation leading to these producers becoming a smaller and smaller share of overall economic output:

https://www.youtube.com/watch?v=DYzT-Pk6Ogw

Now look at finance, and focus in particular on 1971:

https://www.moneyprintergobrrr.com/

We introduce these charts one at a time so as not to overwhelm the reader, but superimposing them gives the starkest impression:

https://en.wikipedia.org/wiki/Not_even_wrong

Pre-1971 money worked, so we needed very little and consistently little finance. But post-1971 money has been completely broken, and so we need ever-proliferating financial services just to make up for all the bullshit injected at the source.

The endgame of this logic is visible whenever an inflationary currency reaches its terminal phase. In Argentina, businesses routinely stockpiled physical inventory—motorcycle parts, raw materials, anything tangible—not because demand justified it but because holding pesos was financial suicide. Warehouses became savings accounts. Entrepreneurs who should have been investing in R&D or expanding production were instead playing a logistics game, trying to convert currency into anything real before it evaporated. A factory owner filling his warehouse with four times the inventory he needs is not engaged in productive capital allocation. He is engaged in self-defense. This is what an inflationary monetary system does to the entrepreneurial process described in this essay: it turns every producer into a speculator on the currency itself, diverting energy away from the innovation that makes things cheaper and toward the frantic preservation of whatever value can be salvaged.

There is, however, a non-coercive way of lowering the demand for money: entrepreneurship. When people exchange money for productive investments like factories, machinery, or R&D, their demand for money falls voluntarily. If entrepreneurs then reinvest profits into further growth, that effect deepens. This gives us a clear distinction. Central bankers try to lower the demand for money coercively by torching its value. Entrepreneurs lower it voluntarily by persuading people to invest in the future. The former makes everything more expensive. The latter makes everything more affordable.

And yet fiat economists remain oddly blind to the distinction. They see a credit collapse and conclude that because prices usually rise when things look fine, and now prices are falling while things look dreadful, falling prices must therefore be the problem. So the central bank must print huge amounts of money to recapitalize insolvent banks and restart lending, such that both the money supply and the price level can resume their ascent. This is not a serious analysis. It mistakes a credit pathology for a price signal. It is also what 99% of professional economists and 110% of central bankers believe.

We have now built enough conceptual groundwork to debunk the absurdity of “stimulating aggregate demand” and “setting the interest rate.” Credit bubbles happen because producers misread market signals or make erroneous forecasts of the future. Artificially stimulated consumption makes them believe demand is sustainable when it is not. They observe attractive paper returns and infer that it is worth investing in more long-duration productive assets of the same sort.

But the apparent demand is fictitious. It does not arise because the stock of savings is already abundant enough that marginal returns on investment have become less attractive relative to present consumption. It arises because money has lied. “Stimulating the economy” is really just forcing people to act on false signals about how much consumption and investment anybody really wants—or forcing them to fear that the value of their savings will otherwise evaporate. The inevitable consequence is a string of investments that later prove terrible because the consumption supposedly supporting them was never sustainable in the first place. It looked as though attractive returns could be earned not merely now but over the whole time horizon required by the project. Then everybody discovers their investments are worthless. Consumption retrenches. Depending on how degenerate the monetary structure is, people may even discover that their “savings” are merely bank liabilities backed by rotten assets. And so the bubble pops.

What creates sustainable consumption is relative certainty, and what creates relative certainty is savings. Savings lower the demand for money precisely because they make one more secure about future purchasing power. The more secure people are, the more their present consumption becomes a genuine signal to which entrepreneurs can sensibly respond. The notion that producers will not invest unless they are nudged by monetary lies is precisely backwards. The nudge produces investment that is more desperate, more foolish, and less informed; or else it produces mere dissipation of wealth on luxuries. Après moi, le déluge.

Consider a toy example. You live in a primitive fishing society. You want more fish for the same input of time, so you decide to build a fishing boat. That means less time spent fishing now, so you must first save fish to sustain yourself while you accumulate the productive asset that will make you richer later. If the boat does not work, or you are terrible at using it, you end up poorer than before, because you both stopped fishing and exhausted your stockpile on a failed experiment. For any of this to make sense, your savings must be real. As Mises notes in On the Manipulation of Money and Credit,

“Roundabout methods of production can be adopted only so far as the means for subsistence exist to maintain the workers during the entire period of the expanded process.”

You need actual fish to survive the period during which you are not fishing. The idea that you would only build the boat if I first stole some of your fish is ridiculous. If I steal your fish, you cannot build the boat. You must go back to fishing. And yet this is the fiat prescription. Apparently, you would not be sufficiently “stimulated” to build a productive asset without the threat of expropriation.

**

Hoisted By Their Own Petard**

“Physician, heal thyself!”

Luke 4:23, King James Bible

Let us entertain one final debunking before wrapping up. Suppose, purely for argument’s sake, that there is some flaw in everything said so far, and that it really is a good idea to “stimulate the economy” by torching money rather than by unlocking real demand through innovation. Suppose that our infinitely wise overlords can know, by whatever mysterious method, that total productive capacity will rise in the long run if they are left to read the entrails in peace; that artificial credit enables worthwhile investments that free capital markets in sound money would miss; and that the increase in the money supply is justified because otherwise the growth would never have happened.

How would we judge whether they were right? What are the hallmarks of a good investment? That after the investment, we are able to produce more with the same inputs. This enables return-maximizing producers to lower prices and take market share. In other words, we would expect deflation. Worthwhile innovation is deflationary, and deflation is evidence of worthwhile innovation. If money exists to price things at all, those are simply different perspectives on the same phenomenon.

One could imagine the scheme being justified as follows: yes, the money supply rose and therefore your share of total purchasing power fell, but productive capacity rose by even more. So although there is more money, it is chasing still more goods. We know it was worth it because prices fell. Again, “falling prices” and “worthwhile investment” are equivalent descriptions of the same outcome.

This cannot fail to be the correct test. If prices are flat after the “stimulus,” the investment achieved nothing. If prices rise, it was a net negative. One could even treat this as a diagnostic test for capital misallocation. Even on the fiat theory’s own terms, we can specify what evidence would be needed to vindicate its prescriptions.

And when one does so, one finds no such evidence. Fiat stimulus has only ever pushed prices higher. It has never, not once in recorded history, produced a provable improvement in capital allocation sufficient to justify the inflation required to produce it.

How do fiat economists explain this? Not by conceding the point. They explain it through a sleight of hand. They switch back and forth between “inflation” meaning the money supply and “inflation” meaning the price level as needed to preserve the illusion of coherence. The trick goes like this:

“We need inflation to stimulate economic growth. Entrepreneurs invest with the new money and GDP goes up, which is good. Prices also go up, but that’s okay because we need inflation to stimulate economic growth.”

Did you catch it, dear reader? Even if one grants all of their insane premises for the sake of argument, the logic still fails on its own terms. Whether they are cynical peddlers of intellectual narcotics or merely intoxicated by their own product is a question for the reader.

Still, do not take our word for it. No serious argument should be accepted on authority. Unfortunately, central authorities have a nasty habit of preventing real experiments in monetary competition. Yet if they are so certain of their system, why not let people choose? Why must hard-money alternatives be corrupted, outlawed, or hemmed in by coercion if the enlightened regime of perpetual debasement is truly superior?

If productivity tends to make goods cheaper over time, and if monetary inflation tends to mask that fact by distorting signals and redistributing purchasing power, then a monetary system that resists arbitrary expansion does something radical. It allows progress to appear as falling prices in the unit of account. This is not “deflationary money” in the literal sense, since the supply schedule may still expand slowly rather than shrink. But it is a monetary base that permits long-term price deflation by resisting human tampering. Under such a regime, saving is not punished, time preference is expressed honestly, investment is financed by real savings rather than fragile or illusory credit, and productivity gains show up as purchasing power rather than being confiscated by dilution.

None of this eliminates business cycles or bad investments. Human beings remain subject to greed and will, at times, miscalculate under conditions of radical uncertainty. But a money that does not lie allows errors to be revealed more quickly. And it allows a person to store the value of his work without being forced to gamble it away in assets or spend it on frivolities simply to outrun the debasement regime of enlightened overseers.

Conclusion

Deflation does not prevent investment. The causality runs the other way. Deflation can occur only where investment has already succeeded—where an entrepreneur risked capital, discovered a more efficient method of production, and passed the savings on to consumers and competitors alike. Investment requires the prospect of returns, returns require sustainable consumption, and sustainable consumption requires a bank of real savings. This is not a theory. It is a description of what happens when entrepreneurs are free to allocate capital honestly.

Inflationary money interrupts every link in this chain. It degrades savings, corrupts the price signals that guide investment, and rewards proximity to the monetary spigot over service to the consumer. The more aggressively it is applied, the more the productive economy is hollowed out and rebuilt as a financial economy whose primary purpose is to hedge against the debasement that sustains it. People still do things, but those things increasingly fail to create value. Capital moves, but it moves in response to fictions, and so it arrives where nobody needs it.

The alternative is not utopia. Business cycles would not vanish. Entrepreneurs would still miscalculate, and capital would still sometimes be destroyed in pursuit of hunches that turn out to be wrong. But errors would surface quickly rather than compounding for decades behind a wall of artificial credit. And the long arc of economic life would bend in one direction: toward a world in which the honest labor of a person’s hands buys more with each passing year, not less.

That is what sound money makes visible. Not a deflationary money in the literal sense, but a money that refuses to lie — and thereby allows the truth of human progress to express itself as falling prices. The number goes down. That is how you know it is working.

*

thanks to @bitstein and Ross Stevens for edits and contributions.*

thanks also to @BitcoinMagazine for the agreement in principle to publish a second edition of Bitcoin Is Venice in 2027, in which we intend the present essay to be a novel chapter.